In 2021, a fleet of water tankers snaked across Taiwan – not to fight a fire, but to keep the world’s most advanced semiconductor facility running. A historic drought had crippled the local water supply, and Taiwan Semiconductor Manufacturing Company (TSMC), the company behind the chips in your phone, your car, and datacentres, was forced to truck in water for four months just to stay operational.

It conjures up a mental image that at first sounds like it belongs in a far-fetched doomsday film, but it happened in reality, just a few years ago, with very real consequences for global supply chains. What’s more serious is that the conditions that caused this emergency haven’t gone away – in fact they’re fully expected to return.

TSMC is one of the most widely held stocks in global equity portfolios. For most investors, it represents exposure to the technology sector. Few think of it as exposure to a Taiwanese watershed, but that’s exactly what it is.

Chips need water. A lot of it.

Semiconductor manufacturing is one of the most water-intensive industrial processes in existence. TSMC alone uses more than 150,000 tonnes of water daily – roughly 80 Olympic swimming pools. And it’s not any ordinary water that’s needed: chip production requires ultra-pure water, filtered far beyond drinking water standards, used to rinse contaminants from chip surfaces at every stage of the process. Without a steady, reliable supply, production completely halts.

Taiwan produces around 90% of the world’s most advanced semiconductors, and TSMC sits at the heart of that. Its ability to keep operating is, in a very real sense, a shared global concern.

The hidden math

In their own 2023 TCFD/TNFD disclosures, TSMC noted the financial impact of physical risks like drought amounted to “approximately less than 1% of revenue“.

While 1% may sound negligible, on a global scale the math is sobering. For a giant like TSMC, with projected 2025 revenues reaching $121.6 billion, that ‘negligible’ percentage translates to a loss of up to $1.2 billion driven entirely by nature-related risk. For investors holding TSMC – whether directly or as part of an index fund – that’s a significant sum tied to a risk that most portfolio tools simply aren’t looking out for or designed to detect.

This is exactly the kind of evidence investors are increasingly expected to surface under TNFD, SFDR PAI disclosures, and CSRD ESRS E4 – frameworks that all push beyond climate to capture nature-related dependencies and impacts at the asset level.

Modelling the shock

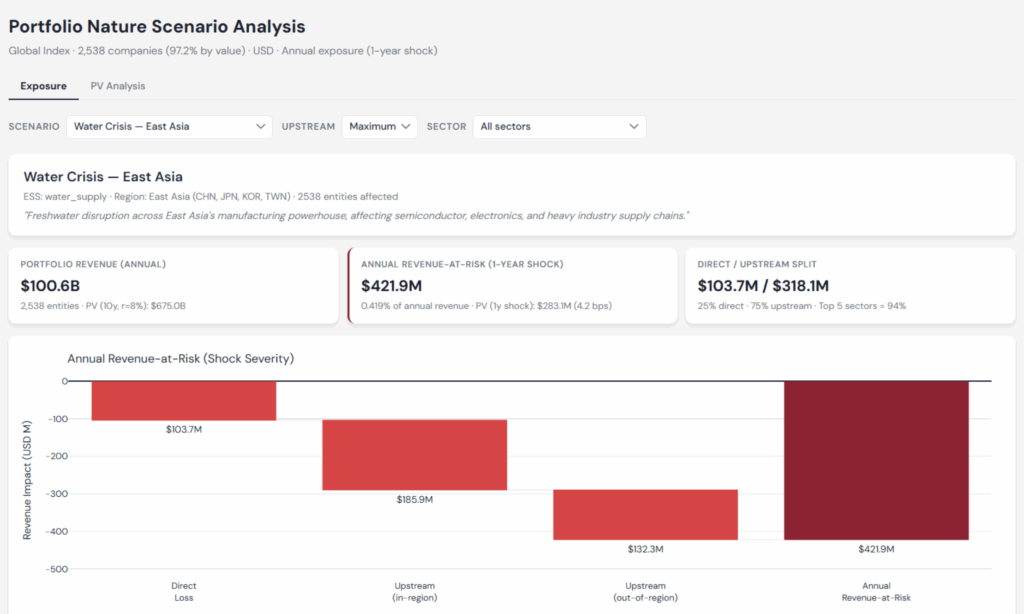

To shed light on these realities, we analysed a prominent global index using Nature Value at Risk (NVaR) – GIST Impact’s framework for translating ecosystem disruption into the language investors already speak: revenue at risk, by company, by sector, by geography.

To measure the impact of a “Water Shock”, we modelled a 1-in-100-year extreme event defined by acute water stress and significant water quality degradation across East Asia.

The takeaway is clear. The majority of nature-related financial risk is “hidden” upstream in the supply chain, rather than sitting in a company’s direct operations.

The geographic anomaly

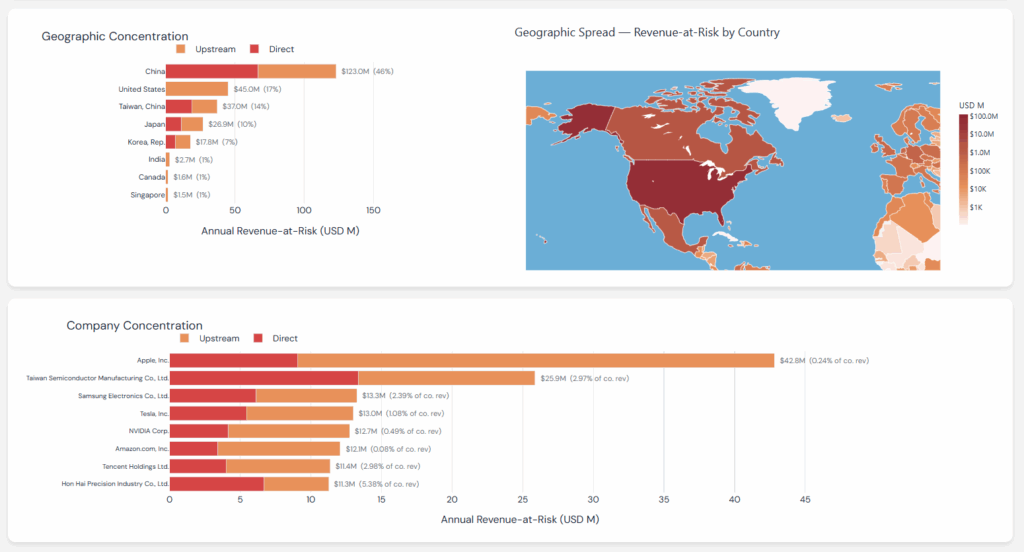

When we looked at which countries carried the most risk, the results were surprising. While China held the highest concentration, as expected, the United States emerged as the second-most exposed country, despite being thousands of kilometres outside the East Asian geography.

How can the U.S. be at such high risk for an East Asian water crisis? A company may be headquartered in the U.S., but its financial health is inextricably tethered to East Asian water basins. If the upstream “faucet” in Taiwan or China is turned off, the downstream revenue in the U.S. dries up.

The asset-level lens

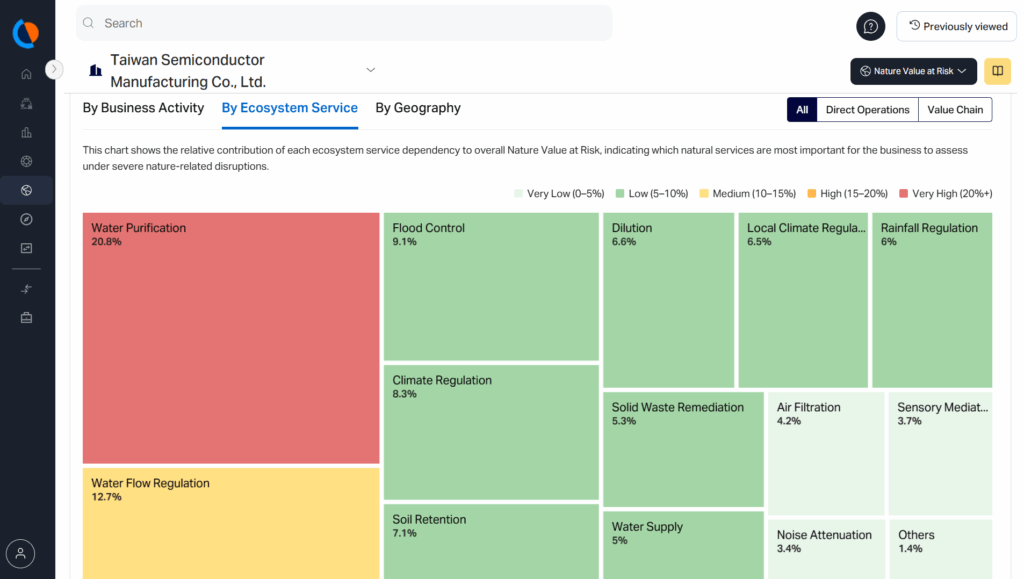

Out of the entire index, TSMC emerged as the second-highest exposed constituent, with 4.02% of their production at risk within this scenario. We then used granular geospatial data to pinpoint exactly which TSMC assets were driving this – and the drill-down revealed that the majority of TSMC’s NVaR is driven by a single dependency: water purification, the watershed’s natural ability to filter water before it ever reaches the plant.

In semiconductor manufacturing, water is more of a precision tool than a commodity. When an ecosystem’s natural ability to purify water is compromised by a regional shock, the cost of industrial filtration skyrockets and operational viability plummets.

And this lens isn’t limited to one stock. The same drill-down can be run across every name in a portfolio, turning thousands of holdings into a mapped, ranked view of where nature risk is actually concentrated.

Flipping the script

By starting with risk rather than just dependency, we shift the conversation from the broad and unmanageable – “We depend on water” – to the precise and actionable: “We have 4% of production capacity at risk at these specific coordinates, because of a reliance on local water purification services.”

The tankers rolling across Taiwan in 2021 were a signal. Whether that signal shows up in an engagement conversation, a risk register, or a new allocation decision, the question is the same: do you have the means to see it in your own portfolio before the next convoy rolls?

—

Get in touch with our team to start your risk-proofing journey today.